Buy Now, Pay Later (also: BNPL) is shaking up the payment market. In 2020, it already made up 5% of annual e-commerce transactions, according to Bain & Company. And the trend is upward, as many online retailers plan to introduce BNPL payment options, as well. The key question for those companies is:

What is the best way to set up a payment system that includes BNPL options?

This boils down to the simple choice between turnkey payment systems by 3rd parties or a custom system built and run in-house.

The first option is quicker and doesn’t require as much domain knowledge and development resources as the second one. However, it comes with disadvantages in the long run such as:

- Continuous fees that cut into revenue

- Dependency on a third party regarding updates and features

- Risk of so-called vendor lock-in, when the BNPL provider cannot deliver the service or changes the price structure, while no alternative provider is available

- Possibility that the BNPL solution in question no longer fits the retailers’ business strategy as it evolves

When building a custom payment system with Buy Now, Pay Later options, these problems can be avoided or mitigated. Companies are even better positioned with an e-wallet system, as BNPL processes can also be built on top of it.

In this article, we provide an overview of how companies can build their own BNPL solution – and why this is even easier with a powerful e-wallet framework.

What Buy Now, Pay Later Does – And Why Customers Want It

When building your own BNPL product from scratch, there is no shortage of stumbling blocks. Your company needs to have enough resources, a development team with proper expertise in financial software and a roadmap and blueprint of the product that matches your company requirements.

Looking beyond that and into the nuts and bolts of typical BNPL solutions, there are 3 major challenges any Buy Now, Pay Later software needs to address:

Making Money (= Getting Paid)

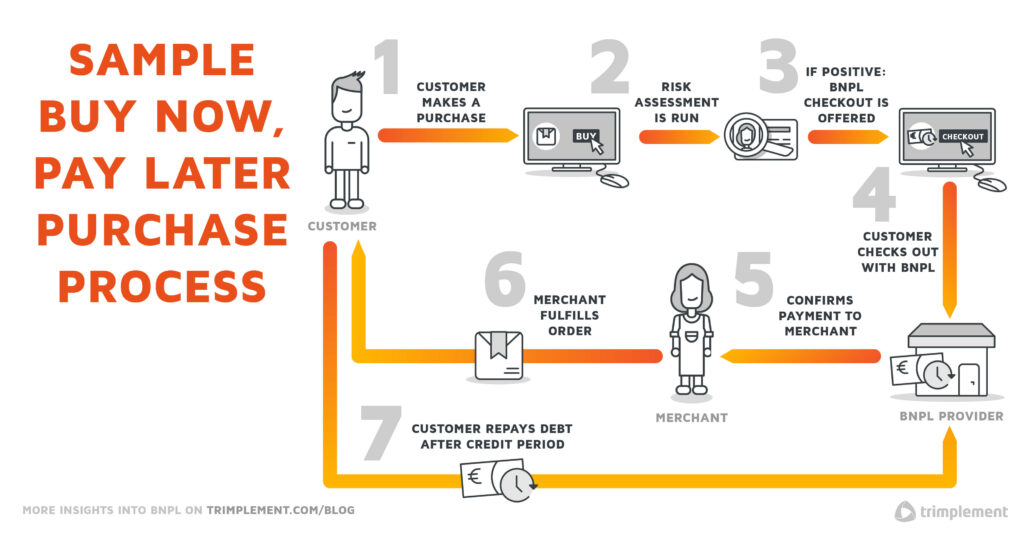

Offering a Buy Now, Pay Later solution means advancing money for customers’ payments. And if you have a marketplace business, merchants are receiving their money as a pre-payment from you. That means, to start a BNPL system, your business must have access to enough financial resources and the appropriate licenses your country’s regulators demand.

What’s more, you have to think about how you want your BNPL to operate and what features and flows it shall have. It starts with incorporating the BNPL checkout flow seamlessly into your payment architecture. Your payment system must be able to handle deferred payments and negative balances of user accounts. Refunding and partial refunding of a BNPL payment is also a big topic.

Once that’s set, you can think about how you want to earn money from your Buy Now, Pay Later service. Most often, we see 3 basic options in place:

- Merchant Usage Fee: This is an option for marketplace platform providers. Here, the merchants pay a fee to the platform provider for offering customers the BNPL payment option. Typically, the fee is a certain percentage of each transaction, plus sometimes a flat fee on top. BNPL-offering marketplace providers often invoice it in bulk at the end of the month. Fees tend to range between 2% and 8%, which would sometimes surpass typical Credit Card transaction fees.

- Interest: Customers will pay the purchase amount + a percentage in interest when full or partial payment is due. Handling accounts that bear interest may require a full banking license. However, most BNPL providers avoid collecting fees or interest from customers altogether. This sets BNPL solutions apart from credit cards and encourages customers to adopt the payment method.

- Dunning Charges: Customers that can’t meet liabilities outstanding will be charged a fee. This is a normal practice for any online payment method. Yet, the fact that some BNPL companies offer the service to financially weak customers and plan with late payment fees as a regular income source has drawn some criticism.

How to Do It With CoreWallet

The CoreWallet framework comes with a feature-rich payment module that can conduct various types of payment actions. Payment actions can trigger different forms of transactions and can be configured and adjusted. This grants you maximum flexibility in your system.

CoreWallet enables BNPL functionalities in two fundamental ways. But each includes a multitude of options for you to tweak the outcome according to your specific business model.

Wallet-Based BNPL

The core of CoreWallet lies within its electronic wallet feature. Customers and merchants can have their own wallets with wallet accounts and configurable limits and usage rights. To set up a BNPL system in this environment, you can allow customer wallet accounts to hold negative balances – under certain conditions.

Thus, when the customer chooses the BNPL option during checkout, the amount for the purchase gets subtracted from their wallet account balance. On the payment due date, the negative balance has to be offset – via direct debit or credit card charge, for instance. CoreWallet handles this as a simple payment action that’s scheduled for a future date – and the system can be configured to send notifications once payment is due or overdue.

Refunds are also easy to manage in this system, as the refund amount can just be returned from the merchant to the customer’s wallet account. The software also allows handling the complexity of partial refunds and refunds for installment payments.

I.O.U-Based BNPL

Instead of giving each customer their own wallet, it’s also possible to record the outstanding balance as a kind of digital I.O.U. A database can be set up to store those, which communicates with the CoreWallet-based system. CoreWallet would then be configured to create an I.O.U. at checkout – every time a customer goes with the BNPL option. Besides, it also schedules a future payment action at the due date, as described above.

BNPL in Installments

In both scenarios, it’s possible to adjust and expand CoreWallet to allow installment payments as well. The system then creates multiple payment actions to be conducted on different, subsequent dates.

Handling Payment Failure (= Not Getting Paid)

Now we know how you get paid in your BNPL system. But what if you don’t get paid – what if the scheduled customer payment fails? Sending out dunning letters after the first default might not prove the best strategy. The inability to pay is not to be equated with an unwillingness to pay.

Instead, it’s better to implement automation and payment orchestration to increase the likeability of payments being completed.

How to Do It With CoreWallet

In CoreWallet, you can set up payment processing to best fit your business model. CoreWallet comes with some pre-integrated payment methods. Yet, you can easily integrate more, including popular, local ways of payment – all of which can be orchestrated automatically to make for a high payment success rate.

What’s more, you can modify payment actions in CoreWallet to react to payment defaults. For example, the system can retry payments at specific intervals or given specific circumstances. Only after several failures, a payment gains the status Failed and CoreWallet notifies the respective parties (i.e. via e-mail or SMS).

You can also set up smart payment routing functions in CoreWallet: The system then automatically chooses the payment service provider with the highest probability of success and the lowest possible costs for the given payment context.

Finally, CoreWallet comes with reporting features and payment history tracking. It can be integrated with 3rd party debt collection agencies, if legal action can’t be prevented. In addition, CoreWallet itself is able to process fines and fees, which are flexibly adjustable if needed.

Scoring and Screening (= Assessing Who May Pay What)

The third challenge of self-created Buy Now, Pay Later systems is at the crossroads of our two former challenges. Some customers have high creditworthiness and their transactions proceed smoothly. Some customers pose risks.

As a BNPL provider, you must be able to always tell those cases apart. Customer screening and scoring are crucial parts of Buy Now, Pay Later to prevent fraud and ongoing payment failures. You need high-performing KYC, fraud prevention, and risk assessment software – not only for onboarding but for continuous monitoring of your customers’ payment behavior.

And when you realize that a customer’s solvency and payment performance is low or decreases over time, your BNPL system must be equipped to react accordingly, setting limits or even denying specific purchases.

How to Do It With CoreWallet

CoreWallet has pre-built KYC processes for customer data verification, e.g. automated email, phone number and bank account verification or manual verification of the personal customer data by admin users using documents uploaded by the customer. Depending on the system KYC configuration CoreWallet can assign different customer verification levels automatically when new customer data is verified through mentioned KYC processes.

Based on those KYC verification levels you can configure allowed actions and different limits in CoreWallet, for example, a limit, that only customers with a certain verification level may pay higher amounts via your Buy Now, Pay Later method.

Through extension points, the CoreWallet framework can also easily integrate 3rd party providers of risk assessment, fraud prevention and KYC services, allowing you to automate/outsource the KYC verification and to have a smart risk and fraud assessment per customer and payment transaction.

BNPL Made to Match Your Business (More Features)

Aside from the features mentioned before, you can mold the CoreWallet framework in any shape you want concerning payment software. Besides the mere basics of BNPL, you can have:

- Wallet Top-Up: Need to implement top-up features on your platform? In a Wallet-Based BNPL system (see above), you can do that. By that, you can enable customers to top up their own wallets. This effectively enables a prepaid flow for future purchases or due BNPL payments, decreasing the risk of payment defaults.

- Various Currencies: Is your platform serving multiple markets across borders? Then you might want to allow various currencies to be applied in the same transaction – including virtual currencies like loyalty points gathered by buying your goods or services.

- Multi-Tenancy Support: Wanting your subsidiaries to use your BNPL system, too? CoreWallet’s licensing options cover such enterprises.

Build Your BNPL Product Now!

At trimplement, we are building custom-tailored payment systems since 2010. Our solutions are in use in more than 50 countries all over the world, offered by large enterprises and financial institutions like Deutsche Bank, PayU, BMW Group, Tide and Delivery Hero.

Send us a request and let’s discuss how we can help!